Over the last few years, India has experienced a silent revolution—not in the streets, but in our smartphones. A few taps and swipes are now enough to buy groceries, pay rent, split a dinner bill, or even donate to a temple. This transformation has been powered by Unified Payments Interface (UPI) and other digital payment methods, turning India into a rising cashless economy.

But how did this all begin? Why is UPI such a game-changer? And what does it mean for India’s future?

Let’s dive in.

What Is UPI?

UPI (Unified Payments Interface) is a real-time payment system developed by the National Payments Corporation of India (NPCI) and regulated by the Reserve Bank of India (RBI). Launched in 2016, UPI allows you to transfer money instantly between bank accounts through your mobile phone—24/7, even on holidays.

You don’t need to know someone’s bank account number or IFSC code. All you need is their UPI ID, mobile number, or even a QR code.

Imagine a wallet that lives inside your phone, and you don’t even have to refill it. That’s UPI.

Why UPI Took Off in India

India’s rapid adoption of UPI wasn’t just by chance. Several factors worked together to make this payment revolution happen:

- Demonetization (2016)

When the Indian government scrapped ₹500 and ₹1000 notes overnight, millions of people suddenly had to switch to digital transactions. UPI and mobile wallets like Paytm stepped in as alternatives to cash.

- Affordable Smartphones & Internet

With cheaper Android phones and low-cost data (thanks to Jio), even rural areas got online. This made it easier for people to access apps like PhonePe, Google Pay, and BHIM.

- Government Push

Campaigns like Digital India and Jan Dhan Yojana promoted financial inclusion. Millions of new bank accounts were opened, enabling more people to use UPI.

- Ease of Use

No need to swipe cards or count change. Scan a QR code or type a number, and the payment is done in seconds.

Mind-Blowing Growth Numbers

- Over 14 billion UPI transactions were recorded in June 2025 alone.

- UPI handles ₹20–25 lakh crore worth of transactions monthly.

- More than 400 million Indians use UPI, from metro cities to small villages.

- India’s UPI is even being adopted by countries like France, UAE, and Singapore.

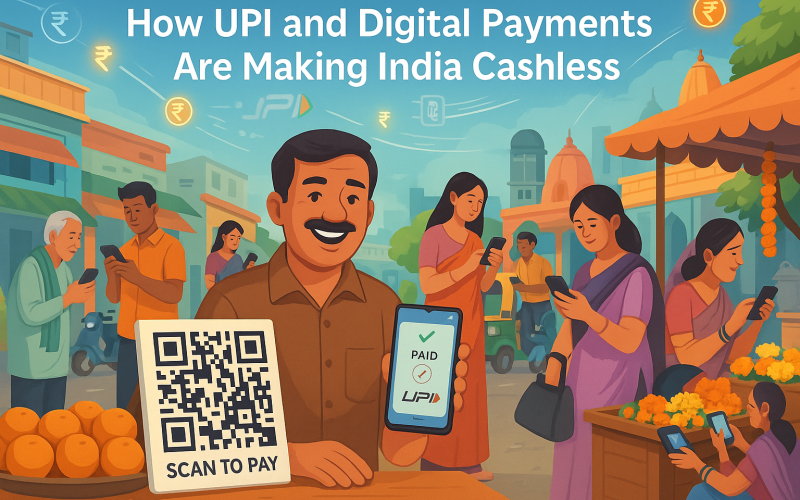

Everyday Examples of UPI in Action

UPI isn’t just for tech-savvy millennials. It’s being used everywhere:

- Street vendors using QR codes to sell chai and samosas

- Small shopkeepers accepting UPI instead of cash

- Friends splitting bills after dinner using Google Pay or PhonePe

- Farmers buying seeds from wholesalers using UPI apps

- Auto drivers and barbers accepting tips via Paytm

Even temples and donation boxes now accept UPI!

Beyond Convenience: Why Digital Payments Matter

UPI isn’t just about ease—it’s about transformation.

- Financial Inclusion

People without credit cards or fancy wallets can now be part of the digital economy. A smartphone and a bank account are enough.

- Transparency

Every digital payment creates a record, reducing black money and increasing accountability.

- Safety

No need to carry cash. UPI apps are encrypted and protected by UPI PINs and biometric authentication.

- Speed

Money transfers that used to take hours or days (like NEFT or IMPS) now happen instantly.

Global Recognition and Expansion

India’s UPI model has caught the world’s attention. The government has signed agreements to link UPI with payment systems in:

- Singapore (PayNow)

- UAE

- France

- Bhutan

- Nepal

NRIs and Indian tourists can now make payments abroad using UPI in partnered countries—making international transactions faster and cheaper.

What’s Next for UPI?

The future of UPI and digital payments in India looks even more exciting:

- UPI for Feature Phones

A new initiative called UPI123Pay enables digital payments through voice-based systems—no internet required.

- Credit on UPI

Soon, you’ll be able to buy now, pay later via UPI, as banks begin integrating UPI with credit lines and RuPay credit cards.

- AI-Powered Fraud Detection

UPI apps are getting smarter in identifying and blocking fraudulent transactions in real time.

- Global Interoperability

More countries are showing interest in adopting UPI or partnering with India’s digital infrastructure.

Challenges Ahead

While the future is promising, some challenges remain:

- Cybersecurity: As usage grows, so do scams and phishing attacks.

- Digital Literacy: Many users still don’t know how to use UPI safely.

- Connectivity Issues: Rural areas still face internet problems.

- Overload Risk: UPI infrastructure must scale to handle billions of transactions daily.

Conclusion:

UPI has not just changed how India pays—it has redefined how India lives. Whether you’re a college student, a rickshaw driver, or a business owner, UPI has made money transfer fast, safe, and incredibly simple.

As we move toward a truly cashless India, UPI stands as a symbol of what thoughtful technology can do: empower people, bridge gaps, and build a more inclusive economy.

So the next time you scan a QR code or tap “Pay Now,” remember: you’re part of one of the most successful digital revolutions in the world.

What do you think?

Have UPI and digital payments changed your daily life? Would you trust it for bigger purchases or international use?

Let us know in the comments—and share this blog with someone still using cash!